Ascend Earnings + Call Notes

Brand leader continues retail expansion.

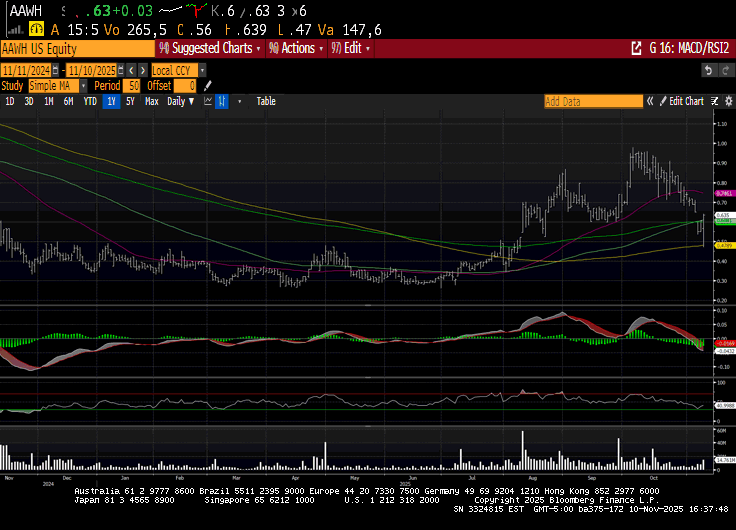

$116.9M Revs; est. $115.5M

$26.3M AEBITDA; est. $23.8M

$44.9M GP; est. $38.3M

$2.5M OI; est. ($5.9M)

38.4% GM; est. 33%

46.1% AGM

Generated Q1 2026 net revenue of $116.9 million and Adjusted EBITDA of $26.3 million

51-location footprint to date, with five dispensaries added in 2026

Ranked No. 2 brand house in Illinois, Massachusetts and New Jersey combined in Q126

Rescheduling poised to unlock immediate and near-term benefits, with potential further impact from follow-on actions

Management Commentary

Our first quarter performance highlights the improved strength of our operational foundation. Amid weather-related closures and a challenging operating environment, our operations proved resilient.

We believe this marks an important inflection point as we execute our 2026 priorities, specifically through further retail densification, the continued enhancement of our customer-first retail model, and the deployment of our CPG strategy designed to capture high-margin sales and optimize our product mix.

Densification puts us on a clear path to drive topline growth in the coming quarters, and we look forward to realizing the benefits of the operating leverage we have built.

Looking ahead, the Trump Administration’s move to reschedule medical cannabis to Schedule III brings real benefits for patients, medical research, and access, while supporting the industry as a whole.

As details emerge following the Drug Enforcement Administration’s anticipated hearing this summer on adult-use cannabis rescheduling, we are encouraged and are actively evaluating the potential immediate and near-term benefits for our operations.”

Call Notes

Cannabis reform shifting,

^ now translated to action with rescheduling announcement

Rescheduling could unlock greater access to capital and financial services, credit card acceptance, and renewed institutional interest.

Actively exploring pathways to uplist to major exchange

Evaluating 280e tax provision given new guidance

Q1 demonstrated resilience in the face of seasonality and industry headwinds

Revs and Adj EBITDA ahead of guidance range and market expectations

Net revenue of $116.9m, down 3% QoQ ; as expected due to seasonality and severe winter weather across northeastern footprint

Favorable product mix increased retail revenue to 71.1% of revenue, up 60bps QoQ ; vertical sales focus

Underlying demand remains healthy, transaction volumes remain stable, sold more units YoY

In markets with consistent pricing, transaction volumes accelerated

Deliberate shift to consistent and transparent pricing, driving higher frequency of visits

Actively replicating pricing model into all markets

Improved quality and appeal of brand, customers are increasingly choosing them

GP fell 1.4% to $53.9m,

Adj GP up 70bps to 46.1% margin

Adj EBITDA of $26.3m or 22.5% margin

QoQ lower sales resulted in reduced absorption of fixed costs

Capital base remains strong, $60.9m cash and no debt maturities until July 2029

Continued driving densification strategy, opened 5 new stores this year, 2 in northeast and 3 in Midwest

Opened NJ dispensary on 4/204 partner store opportunities remain in NJ pipeline

Retail pipeline includes 10 additional stores

Should be at at least 60 stores by YE

Will expand retail expansion past 60 store target

Incremental retail revenue will drive operating leverage and should lead to improved margin and profitability

Customer first retail offering, improving in-store experience ; customers responding positively4.6 of 5 stores google retail rating

Engagement strengthened meaningfully, monthly review volume increasing for locations

Menu refinements prioritizing in demand products

Over 370 retail pop ups during the quarter

Ascend Pay adoption accelerated from 6.2% in Q4 to 8% in Q1, 29% increase

Streamlining payments and enabling faster checkouts across network

Loyalty membership up 34% QoQ

89% of transactions in Q1 tied to Ascenders Club members, who spent 20% more per transaction, visit more often, spend more per visit, and buy AAWH brands vs. others

^ all improves margins

Ascend reached #2 brand house by sales and units in IL MA NJ combined, 3 of the most competitive markets in the country

Moved from outside to #2 in under 1 year, driven by quality improvements and portfolio breadth

NJ MA IL m/share grew 11% QoQ

Infused flower portfolio up 37.5% QoQ

High Wired gained 44% share QoQ, ranked #1 infused flower brand across the 3 states

High Wired superior inputs vs. competition

Reaching #1 in a category is a meaningful result, only introduced High Wired brand in 2025

Ozone flagship brand, after a year of focus/investment to reach highest quality standards

Improvement in flower, strain diversity, and product quality across facilities

Upgraded Ozone packages and visuals in line w/ quality increase

Launched live spectrum Ozone gummies in IL MA NJ

Ozone drove 2.6% vertical sales launch after relaunch

Budtenders now actively recommending Ozone products because they believe in it, a strong signal of genuine brand health

Launched Honor Roll, 100% full flower pre-rolls

Launched High Wired sugar caps and liquid diamond vapes

Launched new King of Queen Cola SKUs

Meaningful developments at state level, including in hemp regulation

Regulatory updates in MA improving market environment, increasing stores to 6 per operator and increasing purchase limits, as well as ownership rules allowing partnerships w/ social equity operators

Could improve MA platform and increase vertical sales of MA platform

Seeing increased ticket sizes post-MA regulation change

Seeing shift of consumers shifting into regulated market vs. hemp market

Licensed operators positioned to compete for share of hemp market demand as consumers shift to regulated market

Densification strategy provides clear runway for growth in coming quarters, will realize operating leverage

$83.1m retail sales, down 2.2% QoQ, decrease driven by holiday spending and seasonality

Pricing pressure across footprint, offset by new stores

$33.8m wholesale revenue, down 5% QoQ

Softer sales in Jan/Feb, offset by orders in March$24.8m cash decrease QoQ,

$19.4m net cash outflows from operations, incl $17m outflows from arbitration Q1 capex of $1.8m in store build outs and $3.4m in cult/manu investments

$20m capex expected FY’26

Majority of facility spend behind AAWH, most now budgeted towards new store openings

Tuck in acquisition capital available to drive densification strategy

Temporarily suspended cultivation operations in Lansing Michigan to remediate a fire, do not expect material impact on MI business

2-3% top line growth into Q2, driven by store openings

Adj EBITDA expected in low-20% range in Q2To date resilience from a volume perspective, consumers continue to buy more, continue to see volumes increase

^ one of the strongest industry wide tailwinds is the consumer

Excited about changes in MA, deliberately pointed that out, will bring health to vertical state operators who can create more density

As get more vertical sales in MA and can grow store count organically and with partners, state should get more healthy

Wouldn’t open more stores in MA, more than enough stores, more of a consolidation play

Stores have outpaced market as a whole, not the barometer for entire markets

Continue to see sales momentum stay strong but cant particularly contribute it to hemp ban, may be a reason but cant say for sure

Hard to quantify portion of business as medical or adult use, all licenses started as medical licenses

Main purpose of ROOTS program isn’t margin expansion, in some of the nation’s most competitive markets, all fighting for customers, all about customer retention and having unique experiences and the right rewards

/end

If you’d like to help Mission [Green] change federal cannabis policies, please click here.

CB1 has a position/ is an advisor and nothing herein should be considered advice.