Since my most recent scribe / deep dive recently published, we’ll keep this light and tight. We covered a lot in that missive and it’s worth a sniff ICYMI, and no we don’t get paid by the click. Shticky but true we’re on a mission to educate and inform as we attempt to capture what we expect will be generational wealth creation as the U.S and global economy onboards a legal and regulated cannabis framework.

Yes I’ve beat this drum for a decade (at times in the dark / freezing cold / while naked, shaking and alone) but the cannabis bull has now massively de-risked and anyone w dry powder / the right risk tolerance stands to make a fortune. I believe that; now we just have to do it.

Per Needham’s industry recap (<-another solid scribe->) “We expect the larger MSOs to average 75% revenue growth and 2.25x growth in EBITDA in '21, and valuation moved from 19.1x to 22.8x estimated '21 EV/EBITDA in the first two weeks of the year. In an industry expected to grow revenue at a 20% CAGR for at least 5 years (MSOs should grow faster than the industry), we aren't overly concerned with valuation, despite the recent run in the group.”

Me, here, now: 2021 #’s are “ok” I guess; now do 2022, 2023…2030 and let’s talk. When I speak of the emergence of a secular bull market / an economic & employment engine – before people are even able to fathom / contemplate that cannabis is more likely to help solve for cancer than cause it— I’m not “trading” the next 10%, I’m positioning for the next 10,000% (give or take).

Funny thing is I used to be grumpy and bearish on the macro when markets were free, so the thought of being cast as the Pollyanna cannabis poster boy is as ironic as it is, I suppose, true—but that’s OK. You gotta be remembered for something in this world so it might as well be for being on the right side of history.

Back to the story. We know four primary metrics drive equity performance– as mapped for our sector in The United States of Cannabis– so we clearly agree with Matty M @ Needham that fundies are FAR from stretched, even in 2021 compares and particularly in the context of the many other moving parts.

“Come for the fundies, stay for the regulatory arbitrages and wait, just wait, till those barbarians bust through those gates” is something I’ve written / repeated often and given how much I hate being redundant (shamefully devoid of original thought) that should tell you how truthful, consistent and forthright I believe that to be.

LET. THIS. SPACE. WORK. FOR. YOU.

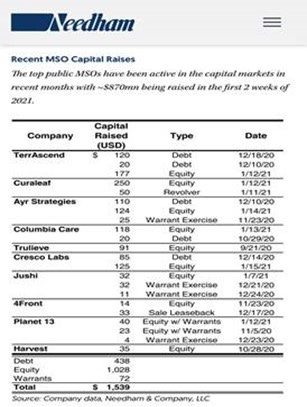

@ the company level, we saw a mad dash to bank-up as the blue paint dried on the Senate. BoJo got the party started but he was hardly alone as close to a billion dollars was raised in the first two weeks of 2021.

Given how uneven the landscape is (private-to-public valuation arbs + distressed properties @ pennies to the public dollars) a literal land grab has emerged as operators look to ratchet down pro-forma multiples through M&A. Obviously the bigger you are the more difficult this becomes and the plush deals will become fewer-and-further between.

Just remember, phase 1 is the “shooting fish in the barrel” / rising tide / influx of money that will raise all boats; phase 2 will determine who the best operators / stewards of capital are. That’s when we’ll separate the wheat from the chaff, the winners from the sinners and the leaders from the posers; the Facebooks from the MySpaces.

There will soon be new meat on the street, with Verano and GAGE gearing up (note: we don’t have a position in Verano as we’ll let it open / trade but it’s expected to be a top-five player; we have a decent position in GAGE through the recent Reg-A).

We view quality supply as a positive as the space opens / democratizes as the magnitude of latent demand currently dwarfs the number of quality US cannabis companies, and intelligent investors will have the opportunity to upgrade their portfolios in real-time.

From a pure positioning standpoint, it remains our view that most US retail / the majority of US institutions have yet to enter the space; this doesn’t mean the upside will be linear, and there will def be turbulence, but if the US cannabis was birthed in 2020, as we suspect, 2021 will be the year of migration.

As Wall Street races to unpack cannabis 2.0, or US-led CPG (not to be confused w cannabis 1.0, or Canadian cultivation), I’ll put my hand up and say “yep, we’re again too early” while pointing w my right index finger toward cannabis 3.0, or efficacy-driven solutions.

This is the biotech pathway that we believe will over time demonstrate an efficacious agility that will help solve some of western medicine’s most pernicious riddles. Follow the science and remember 1. the ECS was first discovered in ’91 (I was graduating the ‘Cuse) and most medical schools haven’t / still don’t include this in their curricula and 2. Western medicine informs the stock market.

Given cannabis research has been stymied by the War on Drugs, it’s not only not priced in—most people don’t even realize this is an emerging sub-sector / asset class that is about to get priced, period.

But alas, that’s a story for another time.

Been reading you since Y2K-ish. Just want to say a profound thank you, Todd, for all the words you put out there while asking for little in return. I've learned the hard way that I'm not a good trader, lol, so I particularly appreciate your longer term perspectives and tweets. I really look forward to being on this journey the next few years with you and the other good people in this space. Gonna be a wild and likely profitable ride.

Thank you 🙏🏼 Great start to hopefully many more substack entries!