It's Time to Exhale

Tax drag to end, earnings will expand.

Note: Cannabis Confidential shifted content strategy in 2026 with insights from trusted partners, industry insiders, and thought leaders who’ve got something to say. There will be no more paywalls or content fees; think of it as The Players Tribune for the cannabis industry, with an ethos of honesty, trust and respect.

Last month, the Drug Enforcement Administration moved to reschedule medical cannabis from Schedule I to Schedule III, setting the stage for a significant shift in the industry’s economic framework.

The most consequential change would be the removal of Internal Revenue Code Section 280E, which has long forced cannabis operators to pay taxes on gross profit rather than pre-tax income.

The key question for both operators and investors is how this regulatory shift will ultimately flow through to financial results—and, by extension, valuations.

In its final rule, the DOJ signaled that the Treasury Department and IRS should consider providing retrospective relief from Section 280E for prior tax years in which companies operated legally under state medical marijuana programs but were nevertheless subject to punitive 280E taxation.

The Treasury Department is expected to address this issue in forthcoming guidance.

The elimination of Section 280E should serve as a meaningful catalyst for increased M&A activity across the cannabis sector, as improved after-tax cash flows, reduced tax uncertainty, and enhanced access to capital markets are likely to support higher transaction volumes and more aggressive consolidation strategies.

____________________________________________________________________________________________

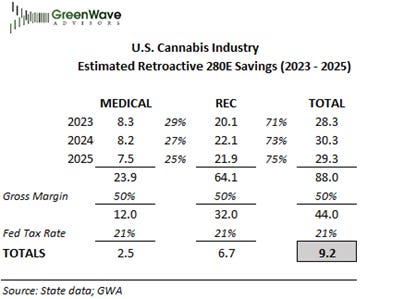

The U.S. cannabis industry incurred an estimated $9 billion in income tax expense attributable to Section 280E during the 2023–2025 period.

Assuming the Treasury Department allows retroactive treatment back to 2023 (a three year look back period), the implications for the top eight operators (defined as the companies generating more than $200 million in annual revenue) could be substantial:

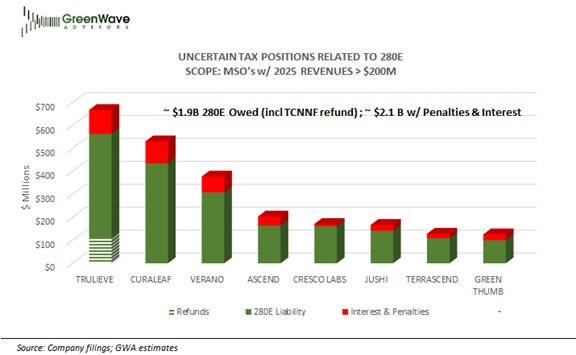

Approximately $1.9 billion of unpaid 280E liabilities have been recorded as Uncertain Tax Positions (UTPs), or roughly $2.1 billion including accrued interest and penalties, portions of which could potentially be waived.

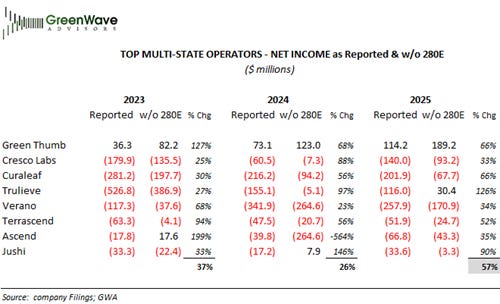

Collectively, these operators could experience an estimated 57% increase in 2025 pre-tax income.

The tax effect of Net Operating Loss (NOL) carryforwards is estimated at approximately $320 million, which could provide an additional incremental boost to valuations if fully realizable under post–Section 280E tax treatment.

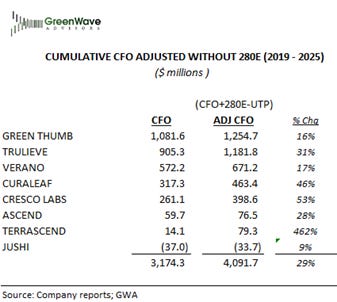

On a cumulative basis from 2019–2025, Cash Flow from Operations would have been approximately 29% higher absent the effects of Section 280E.

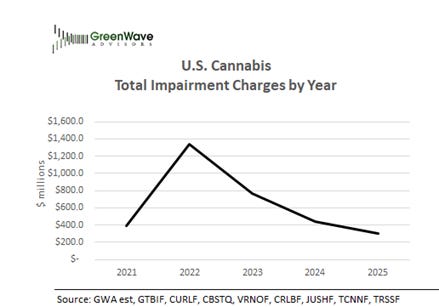

Impairment charges peaked in 2022 and conditions have since improved suggesting that the worst effects now appear to be behind us.

At present, the anticipated tax relief appears limited to medical marijuana businesses, although adult-use (recreational) markets could ultimately receive similar treatment as federal agencies continue broader reforms to cannabis classification.

This approach may reflect the relative ease with which states could convert or integrate recreational markets into existing medical frameworks, thereby reducing or eliminating the need for regulatory separation between the two systems. Such integration proposals are already under discussion in California.

There is no material differentiation in the composition of cannabis products sold for medical versus recreational use, further supporting a uniform approach to the application of Section 280E across state-licensed cannabis businesses.

Applying different tax treatments to medical and recreational operators would complicate accounting practices, create confusion, and increase administrative costs, while also introducing significant compliance risks.

Additionally, it appears that there is growing institutional support for broader application.

The American Institute of Certified Public Accountants, while not determinative, has recommended retroactive application to the beginning of the tax year—a position with which the IRS has concurred that rescheduling will first apply to a business’ full taxable year that includes the effective date of the Final Order (January 1, 2026).

In its final rule, the DOJ signaled that the Treasury Department and IRS should consider providing retrospective relief from Section 280E for prior tax years in which companies operated legally under state medical marijuana programs but were nevertheless subject to punitive 280E taxation.

The Treasury Department is expected to address this issue in forthcoming guidance.

At the same time, the Administrator indicated that Section 280E should be applied consistently to all state-legal cannabis operators, irrespective of whether their activities involve medical or recreational marijuana.

An administrative hearing is scheduled to commence on June 29, 2026, to consider the issue.

Under U.S. GAAP, companies generally account for a favorable resolution of an Uncertain Tax Position prospectively in the current reporting period through the income tax provision.

However, it remains unclear whether that treatment would apply in this context, particularly if future guidance or legislation were to provide retroactive relief or require companies to reassess prior-period tax liabilities associated with Section 280E.

____________________________________________________________________________________________

Uncertain Tax Positions as of 12/31/2025

The Internal Revenue Service generally has three years from the return due date or filing date—whichever is later—to assess additional taxes.

Accordingly, much of the analysis herein focuses on the 2023–2025 period, although that framework is arguably arbitrary, as the practical scope of potential relief could extend beyond those years depending on filing positions, amended returns, tolling agreements, or broader administrative action—though it is equally possible that relief remains confined to a narrower statutory window.

To put the issue in perspective, a rough estimate suggests that making Section 280E repeal retroactive for 2023–2025 could generate approximately $9.2 billion in aggregate tax savings for the U.S. cannabis industry, assuming a uniform 50% gross margin across operators. The estimate is inherently directional and sensitive to assumptions regarding profitability and state conformity.

At present, approximately $1.9 billion in unpaid Section 280E liabilities is outstanding among the eight largest U.S. cannabis MSOs, each generating more than $200 million in annual revenue, for the period spanning 2023 through 2025.

It remains uncertain whether these obligations will ultimately be forgiven or whether companies may qualify for refunds on prior payments. In most cases, the relevant refund and assessment period covers tax years 2023–2025, though for some operators it may extend further back.

Trulieve received approximately $113 million in apparent erroneous refunds related to amended returns for tax years 2019 through 2021 (it is unclear if the IRS will seek repayment). The company ceased paying Section 280E liabilities beginning in 2023.

Net Income Increases – Profitability on the Horizon

As the table indicates, the top eight operators would have experienced as much as a 57% increase in 2025 pre-tax income without 280E.

Improved Cash Flows

If Section 280E had not been in effect, aggregate cash flow from operations for the top operators would have been approximately 29% higher on a cumulative basis from 2019–2025. The benefit could be even greater as other costs associated with federal prohibition decline, including elevated costs of capital, insurance, regulatory compliance, and limited access to traditional financial services.

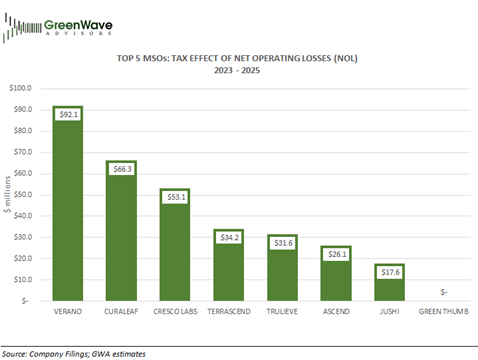

Net Operating Losses Could Boost Valuations

Net operating losses (NOLs) could provide an additional boost to valuations following the elimination of Section 280E. If cannabis businesses are treated in line with other industries, accumulated NOLs would generally become available to offset future taxable income, thereby increasing after-tax cash flows.

From 2023–2025, the top eight MSOs are estimated to have collectively generated approximately $320 million in deferred tax value from NOLs.

If fully realizable, these tax assets would represent incremental economic value that could be incorporated into valuation frameworks, particularly discounted cash flow (DCF) models, as they effectively reduce future cash tax obligations.

That said, the actual value of NOLs depends on several constraints that still apply under U.S. tax rules, including:

limitations on annual utilization (if ownership changes occur),

the ability of firms to generate sufficient taxable income in future periods, and

whether regulatory or legislative changes allow full recognition or accelerate utilization.

In valuation terms, the key impact is that removal of 280E not only improves operating cash flow going forward, but also potentially unlocks deferred tax assets that were previously economically constrained.

Impairment Losses Behind Us?

280E has pressured cash flows and driven significant write-offs. Impairment charges peaked in 2022, as shown in the chart, and conditions have since improved suggesting that the worst effects now appear to be behind us.

This is Third-Party content and does not reflect (or not not reflect) the views of Cannabis Confidential or CB1 Capital.

Matthew (Matt) Karnes has over 25 years of diverse finance and accounting experience. Prior to founding GreenWave Advisors LLC, Matt worked in equity research focusing on the Radio Broadcasting and Cable Television industries for First Union Securities. Matt also covered Satellite Communication at SG Cowen and in addition, worked with the top ranked Consumer Internet analyst at Bear Stearns & Co – this team was consistently recognized by the Institutional Investor’s “All America Research Team”. As a sellside equity analyst, Matt authored and co-authored numerous emerging industry research reports including such names as Google, Sirius, XM Satellite Radio, DIRECTV and EchoStar Communications.

Disclaimer

This investment research report is provided for informational and educational purposes only and does not constitute investment advice, financial advice, trading advice, or a recommendation to buy or sell any securities or financial instruments. The views and opinions expressed are based on publicly available information believed to be reliable at the time of publication, but no representation or warranty, express or implied, is made as to its accuracy, completeness, or correctness.

Past performance is not indicative of future results. Investing in financial markets involves risk, including the possible loss of principal. Readers should conduct their own independent research and consider their individual financial circumstances, objectives, and risk tolerance before making any investment decisions. The author and/or affiliated parties may hold positions in the securities discussed and may change such positions at any time without notice.

Neither the author nor any affiliated entity accepts any liability for any loss or damage arising directly or indirectly from the use of or reliance on this report.

| A guest post by

|

And now, Marty Makary is out at FDA. His exaggerated fears of Cannabis Use Disorder have definitely been slow walking cannabis reform.