Trulieve Jumps the Shark

U.S. operator positions for NYSE uplist.

Recent Headlines

We fired up the Thursday pup to find tech taking it in the teeth as Broadcom dinged the AI trade, an Iran situation that continues to drag on, and our country one month away from it’s 250th anniversary.

Much is expected in the next month-ish for the canna complex but the waiting is the hardest part given how long it’s taken to get to the starting gate. We know what it’ll take for a new bull mkt—growth, regulatory parity, and tax clarity—and all of those items are on seemingly on the horizon.

^ growth is likely a 2027 story post-intoxicating hemp + new state adoption.

Before the open, Trulieve filed an 8K, which ATB digested in real-time as follows:

This morning, Trulieve announced a corporate restructuring designed to segregate its medical-only market operations from its mixed-use (adult-use and medical) markets.

The explicit goal of this move is to pave the way for a listing on the NYSE.

Those familiar with the sector will recognize this playbook as a near replica of the Canopy Growth / Canopy USA structure:

• Trulieve will hold non-voting shares in the non-listable (mixed-use) portion of the business.

• These non-voting shares represent around 90% interest in those assets.

• They can be exchanged for common, voting ownership as soon as federal law or exchange rules permit full listing.

Because this structural precedent already exists, we believe Trulieve is executing this in close consultation with the NYSE. Consequently, we expect an official listing to materialize very soon (management did not provide a timeline).

While modeled after Canopy, Trulieve’s situation is also quite different.

75% of Trulieve’s business is currently done in medical-only markets. Uplisting this portion of the business is now viable due to medical cannabis rescheduling. The NYSE is signaling comfort with listing DEA-registered medical cannabis operations, which is a positive sign for sector normalization.

Note that Trulieve is segregating its assets state-by-state. This clean cut eliminates the complexity of parsing medical vs. recreational revenues within a single state, which likely made the NYSE more comfortable accepting the structure.

Why Now?

We do not view this move as a negative signal regarding the timeline for full federal rescheduling. Instead, we think Trulieve wants to be the first MSO to uplist.

We expect the first to hit a major US exchange will capture outsized benefits from the expected wave of institutional capital and trading liquidity.

This first-mover advantage can support a higher trading multiple compared to peers, even after other MSOs eventually join them. Even if Trulieve beats the rest of the sector to the NYSE by just 2 to 3 months, this premium could be sustainable.

Can other MSOs do the same?

We believe most will wait for full rescheduling. Trulieve’s situation is different because of their outsized exposure to medical-only markets.

Looking across our coverage, Curaleaf could be a candidate for a similar structure. Management is historically more active in pursuit of uplisting (they are listed on TSX). Moreover, their consolidated exposure to medical-only markets (including their large international medical footprint) likely sits around 60%-70%, which is not too far off from Trulieve. However, we don’t know if they would pursue this.

Already NASDAQ-listed, SNDL is another name positioned to secure direct US operations on a major exchange. We expect SNDL to take ownership of Parallel’s Florida and Texas operations sometime in July. We anticipate NASDAQ will clear this, allowing SNDL to begin consolidating Parallel’s financial results.

Ultimately, we believe full rescheduling (which we anticipate by the end of August) could ultimately pave the way for full MSO uplistings without the need for these corporate restructurings. However, Trulieve chose not to wait around and be first.

These are exciting times for the cannabis sector!

Kim’s move is consistent with the theme we discussed last week, where we posited the larger players were moving on up. It remains to be seen if GTI will shift their MMJ into their NASDAQ-listed RYM 0.00%↑ vehicle, or if they’ll wait until the AU ALJ is finished.

Captain Kush 🫡

I spent last night with one of my favorite people in the space after a 3 hour sojourn to and from Red Bank NJ to dine with VFF 0.00%↑CEO Mike DeGiglio. The retired Navy Captain and I go way back and we made good use of our time, and I left there feeling better than ever about his/ their story.

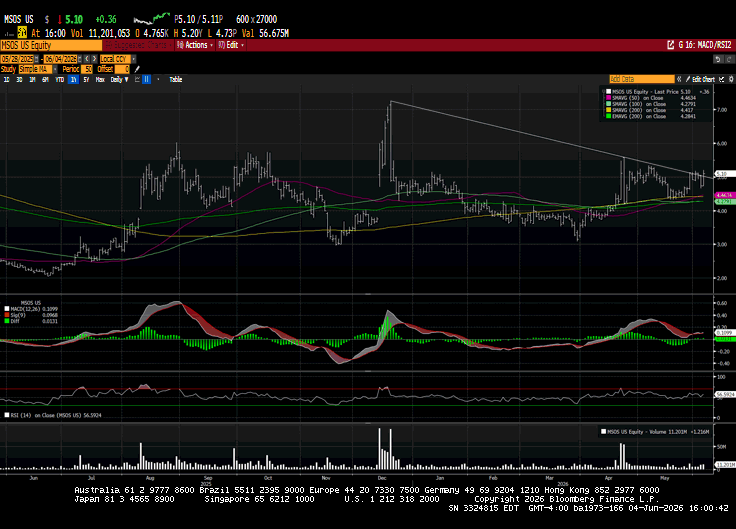

Chart Check: MSOS

The U.S. cannabis ETF has been stuck above the cluster of moving averages/below the downtrend line from the December rug. The $5 strike open interest / 📍 risk remains nto June expiration but the further away it gets, the less of a 🧲 it’ll be.

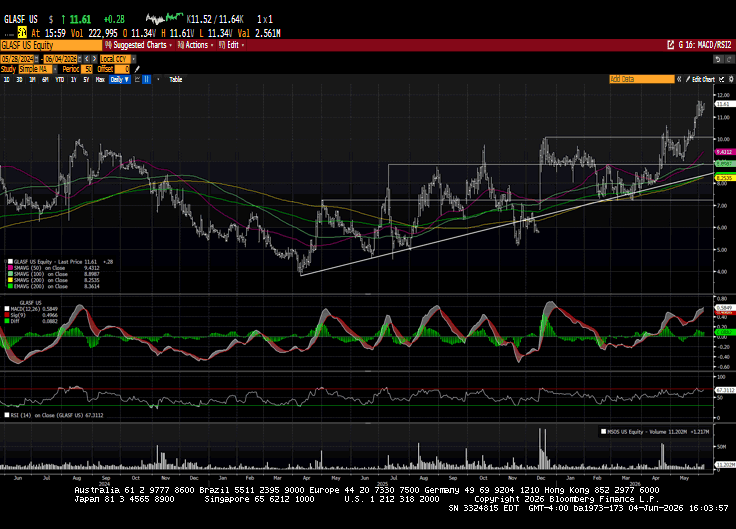

Chart Check: Glass House Brands

With the warrants (struck at $11.49) now out of the way, the GLASF chart is the best in the west, and the east, for that matter.

Top Stories

The FDA Is Quietly Fast-Tracking A THC Drug — And It’s A Big Deal

Can You Bring Cannabis on a Plane? The TSA’s New Guidance, Explained

State budget could provide end-run for Virginia’s retail weed

Massachusetts Legal Marijuana Sales Top $700 Million So Far In 2026

Florida MMJ Sales Top 9.1B mgs Of THC In 2026, Smokable Sales Top 3M Oz

Kentucky Governor Orders Expansion of MMJ Qualifying Conditions

First medical cannabis store opens in Alabama after years of delays

Canadian Cannabis Industry Meets Trade Commissioners In London To Strengthen Global Export Position

Cannabis use grows among young people in Japan, especially in Tokyo

Marijuana status change seen as evolution, not revolution 👇

Industry Headlines

Cohodes & Co. Host Glass House Brands Management 🎙️

AlphaNooner - Cannabis at an Inflection Point: Todd Harrison 📺

TDR: George Archos and Aaron Miles talk Verano and the NYSE 📺

Ethan Russo: The Neurologist Who Changed The Science Of Cannabis

ATB hosted Verano Holdings today:

Business Overview and Q1 Performance

Q1 demonstrated strong sequential top-line organic growth from Q4, with margins stabilizing. Expansion in margin and cash flow is projected for the second half of the year. Strategic focus remains on organic growth and market share, with leadership noting recent “spadework” regarding re-domestication and refinancing. The company maintains a significant operational footprint in Florida, Texas, Virginia, Pennsylvania.

Capital Markets and Up-listing Readiness

Verano completed its re-domestication from Canada to Nevada. While currently listed on the CBOE senior exchange, the company has aligned its board and governance committees with U.S. standards to prepare for a potential up-listing. Recent financial activity includes a $195 million debt refinancing at 9.5% and a $100 million line of credit at 10%. A one-to-five reverse stock split was also executed to meet stock price requirements.

Regulatory Outlook

There is optimism regarding upcoming regulatory milestones, specifically the June 29th hearing and the July 15th deadline for plant reclassification visibility. The company has evaluated alternative up-listing structures to remain flexible but will not pursue an ADR structure.

Operational Details and 280E

Medical sales account for approximately 60% of the retail business. For Q2, 280E savings will be recognized starting from April 22nd. While there is potential for retroactive relief, no official guidance has been released. Verano has submitted all necessary DEA registration applications and continues to manage its medical and recreational programs effectively.

M&A and Market Strategy

Verano has invested in a third facility to prepare for Florida adult-use and has initiated a share buyback. While the company is open to M&A to fill specific gaps, it remains selective. Regarding the anticipated federal hemp ban in Nov, leadership believes it could be a significant win for the regulated cannabis space, though the impact will depend on state enforcement. International remains a “wait and see.”

AGP on Trulieve

TRUL Makes The First Move As it Separates the Business to Prepare for NYSE Uplisting

Earlier today, TRUL announced that the company has deconsolidated its dual-use (adult use and medical) operations from its medical-only state businesses, as part of an effort to apply to list on the NYSE.

The structure of the deal is similar to that of Canopy Growth and Canopy USA, where the company’s operations in dual-use states will become part of NewCo that TRUL holds a 90% economic interest in, and right to consolidate upon permission from NYSE.

While we had recently spoken to an expectation for most operators to wait until potential phase II of rescheduling (whole plant vs just medical-only states) and whether that allows for entire businesses (including adult use) to uplist, TRUL is in a unique position given its weighting current operations being in medical-only states (75% of 1Q26 sales) and it has key catalysts in medical-only states given TX and GA that have both recently expanded to a more comprehensive medical program.

Importantly, management noted this decision was not indicative of its confidence in whether Phase II rescheduling (whole plant) comes to fruition, but rather provides optionality as the company will still be able to consolidate the adult use business if permitted by NYSE (post whole plant rescheduling or otherwise).

We view key things to watch include, if/when TRUL gets approval for NYSE listing (which we expect given it now consists of DEA-licensed operations), as well as the impact of uplisting, including inclusion in indexes, improved liquidity, institutional ownership and potential strategic investments (from CPG, pharma or otherwise).

Despite our view that TRUL is in a unique position, we’ll be curious to see if this pushes other companies to be more proactive in looking to uplist their medical-only businesses versus waiting for Phase II rescheduling (whole plant) that could potentially allow for entire companies being able to uplist.

Within the medical-only business TRUL will continue to consolidate operations within FL, PA, WV, and GA, along with potential operations in TX (conditional) and AL (held up with litigation).

Meanwhile, NewCo Harvest will consist of operations within AZ, OH, MD, CT, CO. The company broke out pro forma financials, which show now medical-only TRUL made up 75% of 1Q26 sales (76% of 2025) and a greater 81% of gross profit (82% for 2025).

Maintain Buy Rating and PT

We maintain our Buy rating and $27 PT on the stock. Our PT remains based on an enterprise value of ~9x our 2027 EBITDA estimate, which is still inclusive of dual-use operations as mentioned above, given TRUL retains a 90% economic interest.

Stems & Seeds

How Cannabis Compounds May Help Create Weight-Loss Drugs

Please Help Scott’s Family in his Fight against Pancreatic Cancer

Have a safe journey, please enjoy responsibly.

If you’d like to help Mission [Green] change federal cannabis policies, please click here.

CB1 has positions in/ advises some of the companies mentioned and nothing contained herein should be considered advice.