Hold on Loosely

A wild ride greets the second quarter

A fortnight ago, we delved into the Bulls, Bears & F*ckery.

Last week, the gloves came off for The Final Battle.

This week? IDK, it’s been fairly quiet. There was that thing in New York...

Some noise in New Mexico…

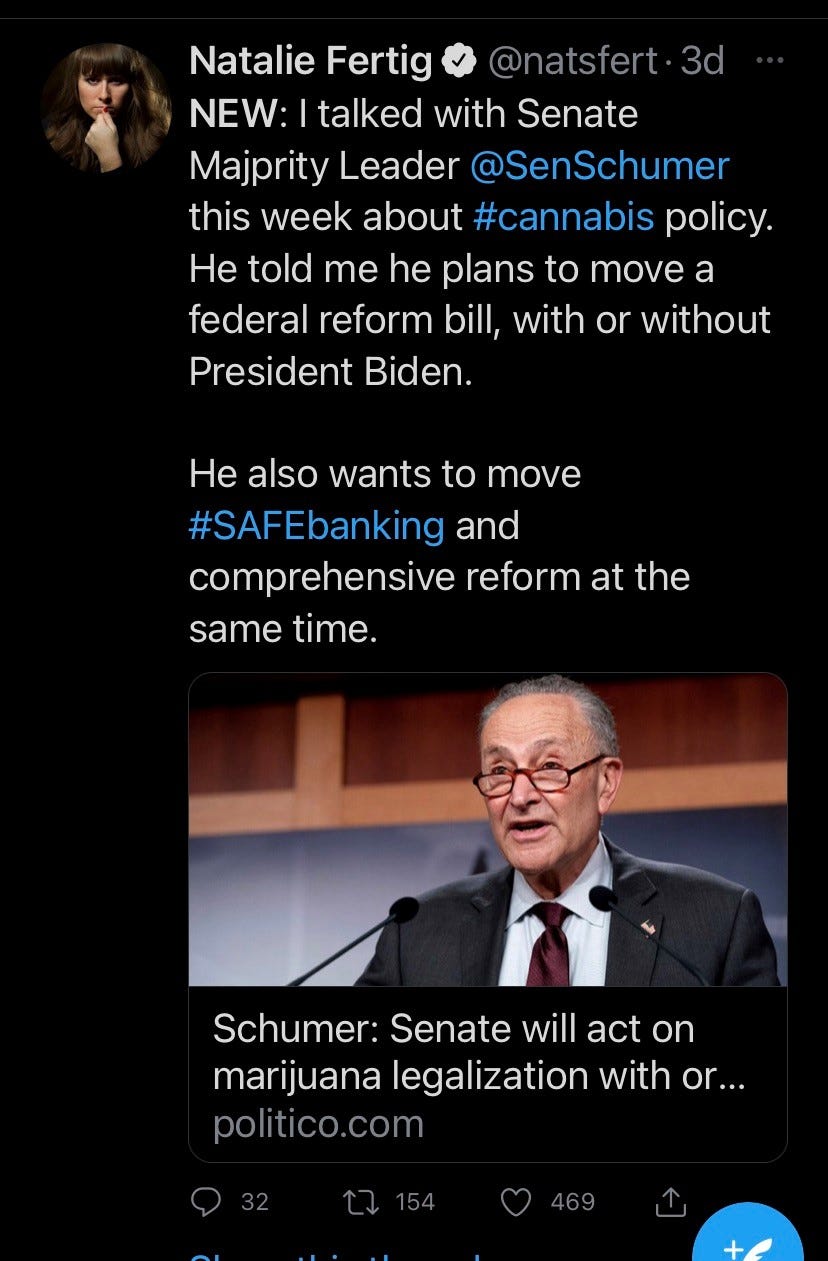

Banter on the Beltway…

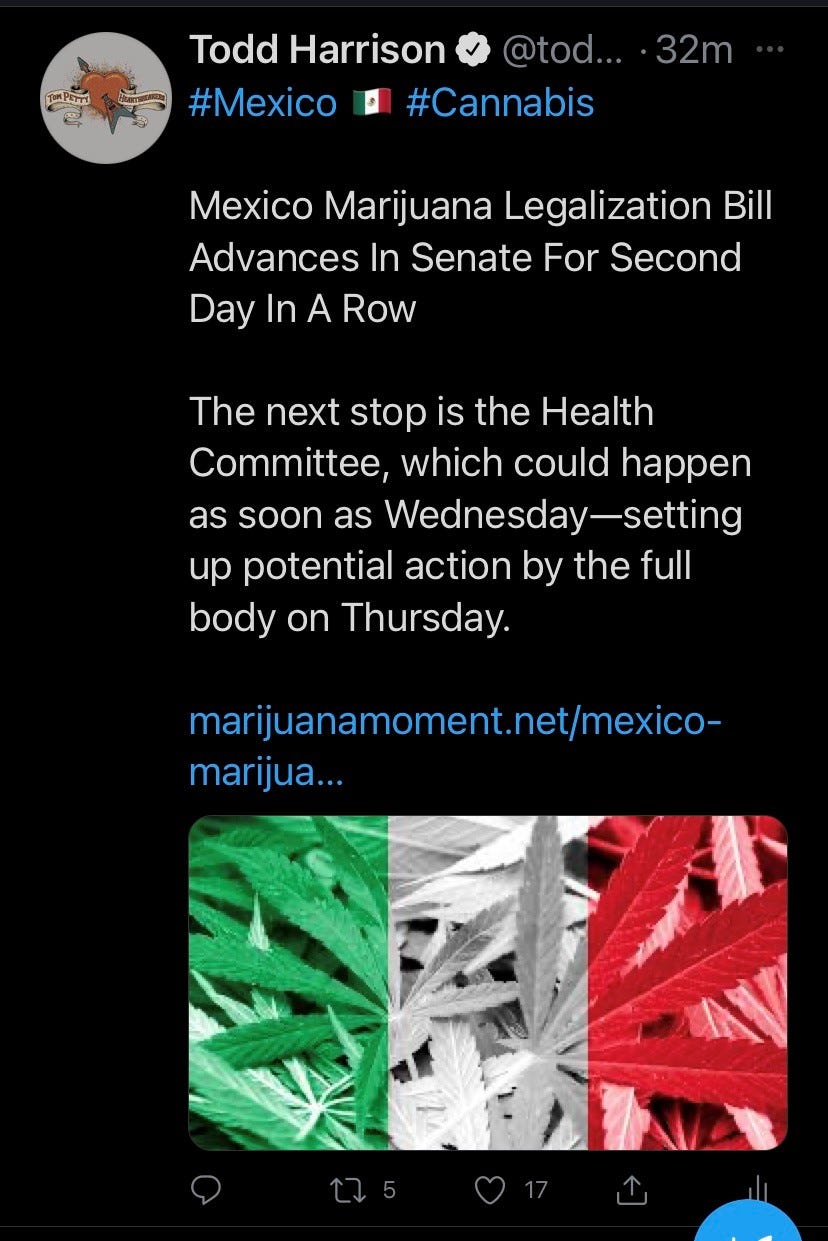

Movement in Mexico…

And one of the Koch brothers joined forces with Snoop Dogg…

Wait, wut? The Dem in the White House is firing peeps for puffin’ and a Koch-bro is rollin’ down the street smoking indo? Hey, you in the back with those French braids…

Where does it all leave us? A quick channel check in Illinois seems to suggest that the first quarter ended strong… to quite strong.

But is it translating to stocks? Or is that thing happening?

[note: given our fakakta reality where U.S operators are listed in Canada (+ pink-sheets) and Canadian LP’s are listed in the U.S, the resulting custody issues / inability of most U.S retail / institutions to access these securities continues to skew traditional tells and mute liquidity; light volume + heavy agendas = these stocks get pushed around]

Step into the Dome of Truth for the “facts aren’t insults” segment of today’s note and understand I’m not doing this to hurt you or be difficult. We always wanna see both sides, even and especially when we’re betting against it.

Broader tape is screaming “risk-on” but U.S canna can’t get out of its own way.

The news has been great— but isn’t news always best at the top?

The reaction to news has been for shit for almost two months now.

Let’s look at a few high-profile examples.

U.S cannabis ETF $MSOS (+17% YTD / -23% vs. 2/10) breached the lifetime uptrend last week / briefly triggered ominous-looking dandruff before bouncing on the NY news. It’ll open this morning above that uptrend but the bears see what we see and will try to break the will of the (retail-dominated) bull-pen by pressing the charts.

They’re prolly leaning against that GTI f*ckery, too. Quick factoid from A. Friend: "Early 2019 was trough valuation for U.S canna @ 10x EBITDA and last wk, $GTBIF was ~10% from that low with a far healthier company / industry and definable near- and long-term catalysts." (looks flaggy > previous ATH to me)

Trulieve even threw 4.4 million shares at the market (pricing tonight for tomorrow) to fortify their war chest and perhaps do some shopping along the East Coast, but that supply is testing the uptrend and will color those who guide themselves accordingly.

What gives? Maybe it’s… Perhaps the… Wait…

Ha, it’s not and we really don’t need to overthink it. As this asset class transitioned from cannabis 1.0 (Canadian cultivation) into cannabis 2.0 (U.S-led CPG), folks got too giddy, stocks ran too far and a few of us had performance muscles going. And when we don’t stay humble in this business well, the market does it for us.

But consider this:

Our best-case three months ago under Mitch McConnell— continued state-level adoption, a status quo federal landscape, the specter of SAFE Banking—is now the base-case. All the while, incumbents continue to build brands, scale and MOAT while their competition is kept at bay.

Our worst-case a year ago was extinction. True story; U.S canna almost got stuffed before it got started by the motivated agendas satisfied with the status quo. U.S canna already raised Billys, most all are turning profits (despite silly taxes and regs) and the smart ones are bolting on accretive acquisitions.

California. Illinois. New York. New Jersey. No matter what happens in D.C, federal policy will coalesce around states’ right to regulate who is allowed to grow, process or sell cannabis. This is an economic and employment need, there’s no turning back and ~2/3 of the country => US canna TAM-in-Waiting.

Plus, if I were a betting man, I’d wager Chuck Schumer will unveil his master cannabis plan by 4/20 because, you know, it’s funny or something. Knee-slap or not, it’ll attempt to protect states’ rights and address social justice, interstate commerce and the role of the FDA. It’ll be ambitious af and opposition will be noisy as hell.

Here’s the thing: most of us knew this is coming and some of us have been waiting for it since January. I can’t tell you how canna stocks will settle on those headlines (would think the first move is higher), I can only say that we won’t know the results of any legislation until late summer / early fall, nor will we know when the market will begin to price-in those potential outcomes. (<-entirely more impt).

Earlier this year, I wrote, “Not sure where the next 30% for U.S cannabis stocks is but I’ve got a good sense where the next 300% is.” The only things that changed since then were prices, which are down considerably, and fundamentals, which continues to improve as the TAM surges (NY alone will add ~20M residents / ~265M visitors (2019))

We’re not betting on the collapse of the federal arbs but when they smooth—banking, tax rates, debt financing, institutional investors—the migration will be massive and the sector will re-rate higher, supported by the fundies and driven by efficient market forces as global institutions onboard exposure for the first time.

Lest you think I’m getting high on my own supply, others see it also, even some U.S banks, which are itching to put a shovel in the ground on behalf of U.S operators.

Can’t blame ‘em. If I saw a trillion-dollar industry taking shape, I’d want in too.

Best advice I can offer is to sync your time horizon and your risk profile. If you’re an active trader, have at it, just be conscious of the liquidity, or lack thereof. If you’re a long-term investor, just follow the fundies and don’t concern yourself too much with the vicious vol; pick your spots, use price to your advantage and hold on loosely.

PS- pro-tip: watch for volume as that will help qualify the intentions of the market.

/positions in stocks mentioned /advisor $MSOS