I did something last week that I hadn’t done in a while; I got away. It wasn’t the best-timing work-wise but when your wife finds a few days that are a fortnight post-vaxx and nestled between SAT’s and lax practices—with school in virtual learning—you, or at least I, just smile, nod and be thankful for some quality vibe time with the family.

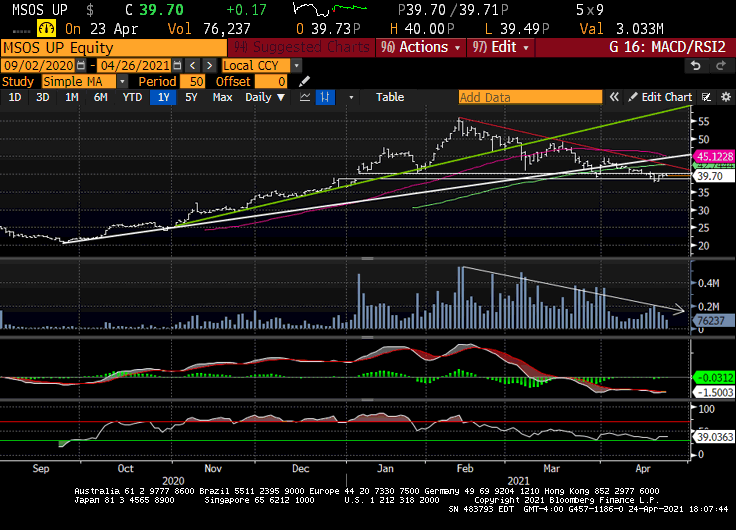

Before I left, we assessed the Growing Pains in US canna and wondered aloud what might be lurking to validate the forward-looking discounting mechanism that is the stock market and the harsh sector correction since the Feb highs. US canna ETF $MSOS maybe +9% YTD but it’s the 29% 10-week decline that has tongues wagging.

Ask those in-the-know why U.S canna suddenly dried-up and you’ll get a familiar retort: that the federal treatment of cannabis as a Schedule I narcotic has, in addition to numerous other impediments, created custody and clearing issues that prohibit institutions / most U.S retail from owning these stocks. And that’s totally true.

But what if something more pernicious is afoot? Did the landscape somehow shift to alter the underpinnings of this trillion-dollar industry in-waiting? Have the vehicles chosen to capture this generational opportunity changed? And if these stocks can’t run with the market on a moon-shot, what’s gonna happen when that script flips?

All worthy questions, even if we can’t yet see the answers.

I’ve been operating under the assumption that fast money took a hella election trade, the die-hard diamond-hands are already all-in, and with institutions locked-out, the marginal buyer is awaiting further clarity on the federal landscape. Factor in the new supply—GAGE, Ascend, GlassHouse, to name a few—and well, here we are.

While there may be more to the story—we heard last week that one of the institutions that was able to accumulate sizable positions in US cannabis got a compliance tap on the shoulder and was forced to liquidate—we won’t know whether that’s true until those filings are released this summer, long after the point is moot.

[note: Seperately, Putnam, the ~$200 billion Boston-based investment manager, filed as a holder in Green Thumb (136,000 shares), TerrAscend (800,000), Columbia Care (626,000) and Trulieve (90,000), and TIAA-CREF (!!) filed as a holder of Green Thumb (165,000), all as of 3/31/21, so the custody landscape remains uneven, at best.]

Either way, I see what you see: a sector that hasn’t been able to rally with the tape and perhaps more troubling, a dearth of trading volume. What’s more, the price action has served to illuminate the duration mismatch between the impatient traders watching in real-time and policy initiatives that will certainly take time.

Great Expectations

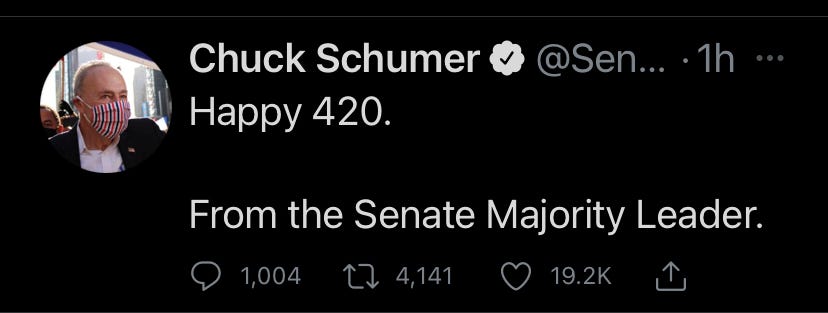

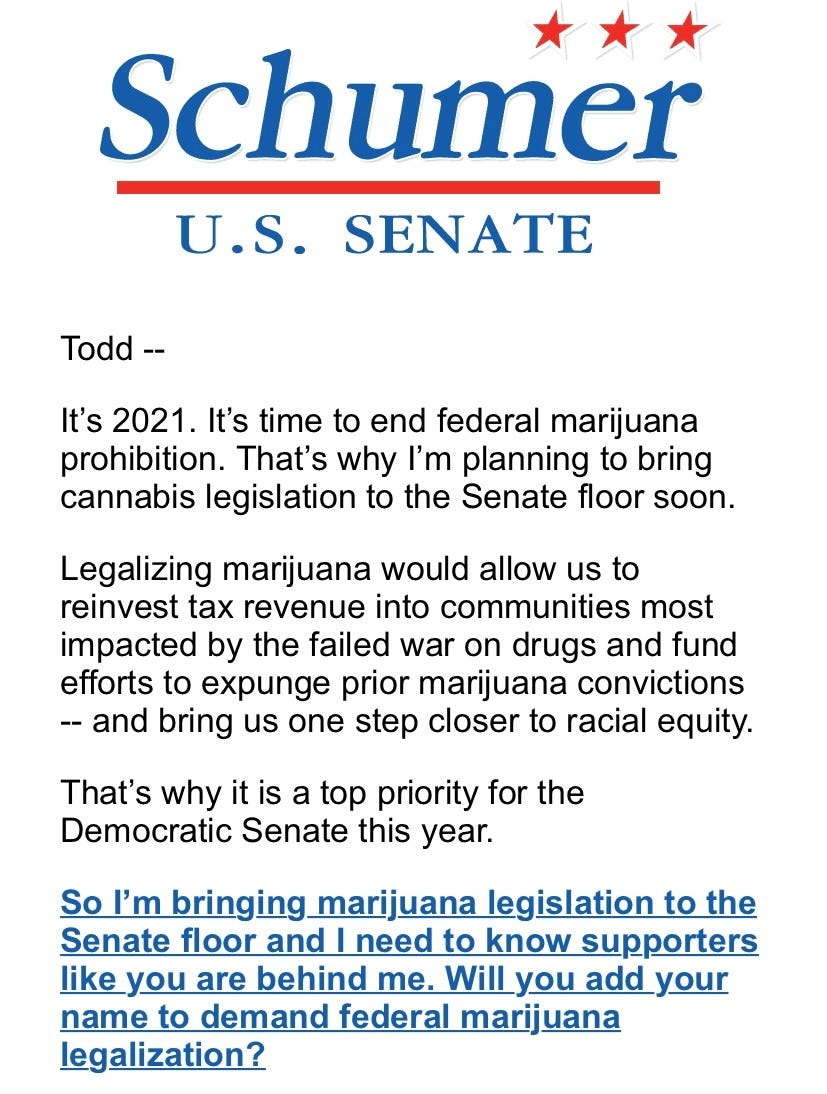

There was alotta hype heading into 4/20 and while SAFE Banking passed the House for a fourth time (321-101), all eyes were on Senate Majority Leader Chuck Schumer, who’s been saying since late January that federal cannabis reform will be his magnum opus.

So what did Chuck deliver? More words, mostly; he called 4/20 an unofficial American holiday, and said that he hoped there will be meaningful reform in place by next year.

The part that wasn’t said, but what the market already knew, was that SAFE Banking would be an integral part of his yet-to-be-unveiled master plan as he’s gonna need those votes to get it passed—and that pretty much puts it on ice as a stand-alone bill.

This prolonged / riskier approach has been priced into U.S cannabis these last few months; it’s why stocks are back at levels last seen when the Senate first flipped.

[note: for fantastic / must-read insight on the cannabis legislative process, click here]

The week-over-week decline in US cannabis ETF $MSOS was marginal, down about a percent, but the disappointment among investors was palpable.

Is the broader bill a pipe dream?

What type of restrictions will be included?

And what if Uncle Joe’s Kryptonite—Schedule II—allows the FDA to rule the roost?

What do I think? Glad you asked. Some Random Thoughts, in no particular order:

Schedule II is a non-starter. You can’t decriminalize cannabis and reschedule it to be like cocaine. It doesn’t work. It doesn’t even make sense.

Descheduling = “decriminalizing” (federal lexicon) = “legalization” as a states’ right = the only legitimate pathway for broad-based criminal justice reform.

Removing cannabis from the CSA will have immediate implications for things like 280E and U.S exchange listings; protecting states’ rights will ring-fence the current infrastructure of multistate operators (MSO’s).

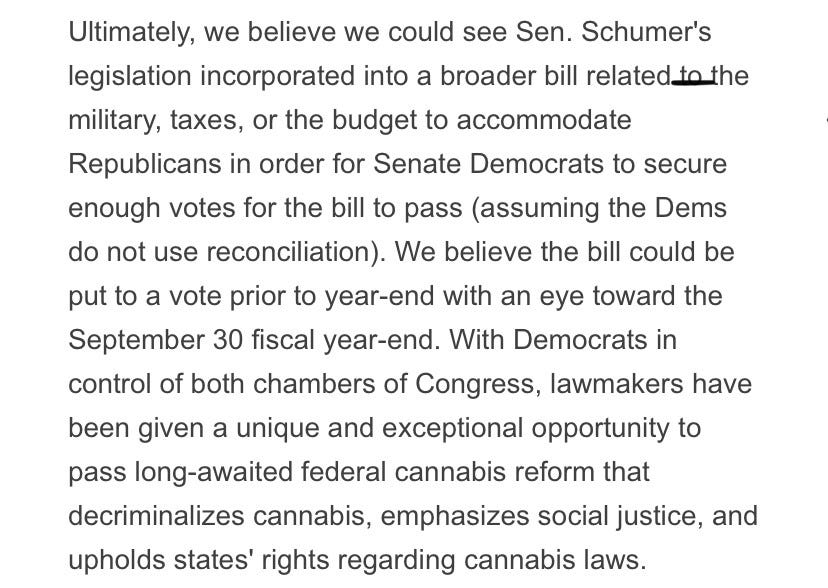

I don’t trust politicians as a matter of course but Chuck made cannabis reform his legislative priority and while I don’t know how he’ll get there, I do believe that he will. BTIG had an interesting thought here, as well:

There is, of course, the chance that he / they can’t get the votes and he / they will dangle this carrot into the mid-terms because, you know, politicians can be like Janice Rossi, who lives in apt 2R.

I’m not sure it matters. Remember, U.S cannabis leaders are making bank despite widespread f*ckery and the longer the feds take to get their act together, the better it is for existing operators as they build brands / MOAT / enterprise value.

And let’s be real, there’s only one way forward…

Given the steady parade of new states that will drive the TAM higher…

And the… come on man! Show me another other asset class growing this fast, generating this many jobs, and providing social utility, at these ‘22 multiples.

Listen, I’m not gonna sit here and say, “heads we win / tails they lose” bc markets don’t work that way; risk doesn’t work that way, and if there weren’t risk, it would be called “winning,” not “investing.”

But I can tell you that absent Schedule II—which again, won’t happen, not only bc it makes no sense, but bc states need tax revs / peeps need jobs in a post-pandemic world (<- also why interstate commerce s/b a few years out)—this’ll work itself out over time.

I can also tell you that perspective is everything. Many are disappointed by the perceived lack of movement on the federal front—and yes, the recent decline in share prices—but I’ll again offer that we could live 50 lives and never be as lucky as we are now, timing-wise. This is historic stuff, just take a giant step back.

Nobody knows what the future holds and I can’t tell you if these names trade to their respective 200-day moving averages; but the best-in-breeds have been on sale as earnings season approaches. We’re talking 30-40% off on the US Canna FANG-type names.

If you’re new to cannabis, check this out, and in particular the research studies by indication / ailments. Cannabis 1.0 was Canadian cultivation. 2.0, where we are now, is U.S-led CPG (canna as an ingredient). 3.0, efficacy-driven solutions, is gonna blow your mind; just watch, and follow the science.

/positions in stocks mentioned

/advisor $MSOS